In Charles Duhigg’s acclaimed book, The Power of Habit, there’s a section that delves into the mundane yet essential act of brushing teeth. This simple habit isn’t driven by our love for the act of brushing, but rather, by the rewarding sensation of freshness we experience afterward. The payoff is instantaneous – a quick, tangible reward for a less than appealing action.

Habit formation revolves around a simple cycle: cue, routine, and reward. This loop, referred to as “The Habit Loop” in Duhigg’s narrative, becomes successful when the span between the cue and reward is minimized. Our innate desire for instant gratification propels us into solidifying routines once the reward is realized.

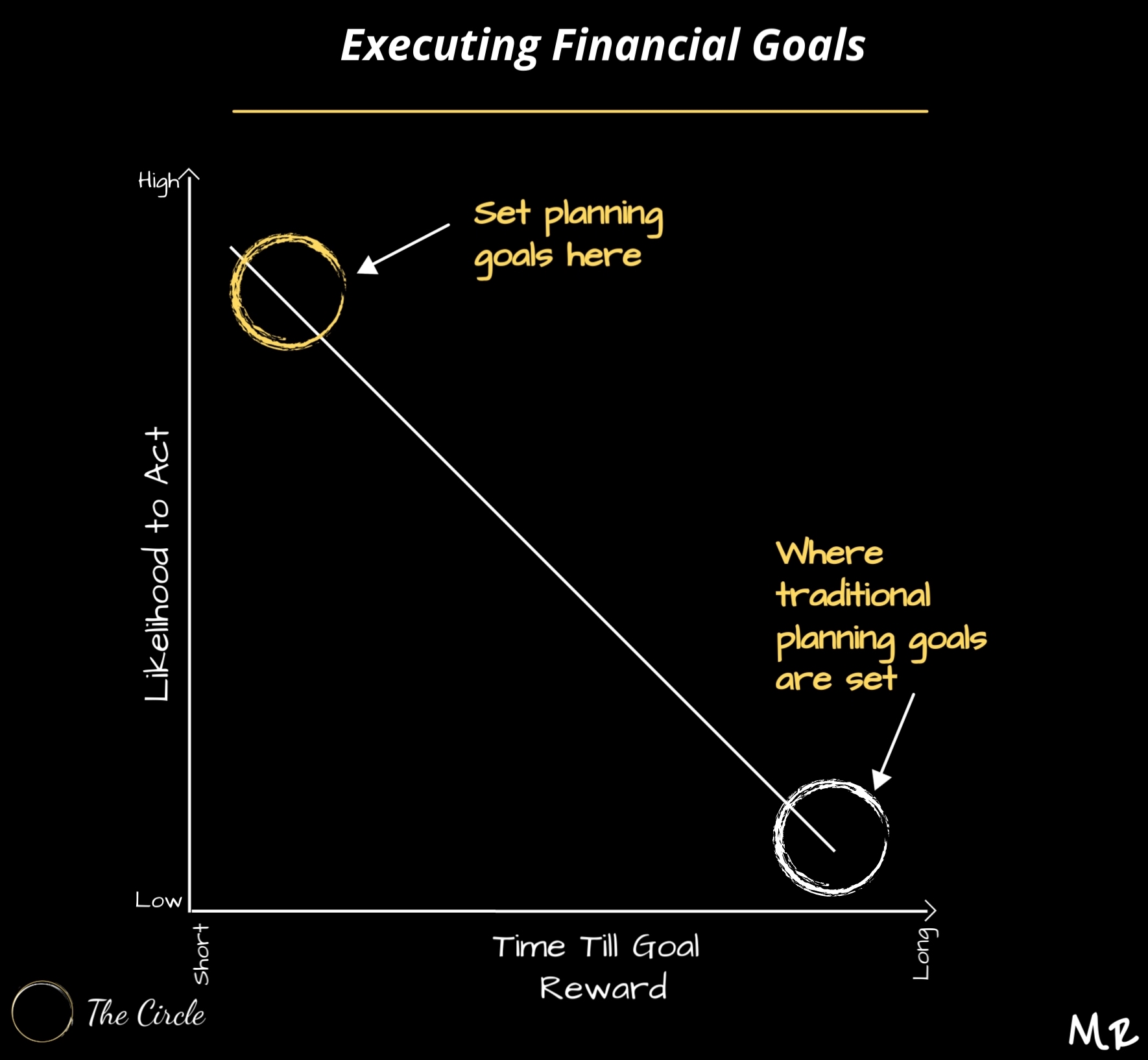

The challenge with financial planning lies in the vast gap between the cue and reward. Take a 30-year-old saving for retirement, for instance; the cue arrives when the paycheck is received, fostering a desired habit of saving in a 401k, but the reward (a comfortable retirement) is a distant 30 or more years away.

Stacking wins is key to habit formation and adherence to a plan. Execute the act (brush your teeth), reap the reward (enjoy fresh breath), and you’re inclined to continue this pattern. However, identifying these win stacks in financial planning is elusive, which often impedes our adherence to and complete execution of a financial blueprint.

Our aversion to change also has evolutionary and neurological roots. In prehistoric times, straying from known territories or experimenting with unfamiliar food could spell death, hence we stuck to known areas and tested foods. Our brains are not naturally predisposed to learning new things as it considerably drains our energy. Given that the brain already consumes about 20% of our energy, the additional exertion of creating new neural pathways further escalates energy consumption, prompting us to revert to familiar, energy-conserving behaviors.

This inherent penchant for the status quo makes the rapid pace of change and innovation in contemporary times particularly daunting, especially for older generations. To transcend this barrier, we must outsmart our instincts, and that begins by understanding our natural tendencies. It’s not about confronting our inherent traits head-on, but rather, devising strategies to outwit them.

Logical appeals often fall flat. The allure of a well-crafted financial plan may appeal to our rational selves, yet our brains, driven by ingrained instincts, often resist change. Hence, simplification is crucial.

In his bestselling book Atomic Habits, James Clear presents a potent tool – the 2-minute rule. The crux of this concept is to distill a large goal into the smallest possible action, an action that takes less than two minutes to complete. For instance, eschew the lofty ambition of running an hour every other day; instead, aim to put on your running shoes at a designated time. This simple act of starting is a gateway to forming enduring habits.

The paralysis often induced by grandiose goals can be alleviated by initiating action. Establishing a cue that triggers a habit eventually leads to a rewarding outcome.

Within the realm of financial planning, setting monumental goals like retirement or a house down payment can be overwhelming. The prolonged duration before reaping rewards often undermines motivation. The solution? Fragment these long-term objectives into digestible, short-term actions.

Consider a couple saving for a house. The modest act of transferring $5 daily at 8 am from one account to another could be their starting point. It’s a task requiring less than two minutes, yet over a month, a savings habit is fostered. While the savings amount will need to incrementally increase over time, the foundational habit of transferring money has been established.

Remember, financial planning essentially entails a current self-investment for a future payoff, an endeavor quite against our evolutionary grain. Our instinctual cravings for immediate gratification often thwart our best intentions for future security.

The discourse surrounding these instinctual behaviors isn’t about right or wrong; it’s about acknowledging reality and devising a strategic blueprint to help clients transcend these barriers.

The foundational framework to propel our clients towards their financial goals commences with setting simple, attainable objectives governed by the 2-minute rule. With this approach, we align our strategic financial planning with inherent human behavior, significantly enhancing the probability of attaining long-term financial objectives.

{kind=link}